Money laundering, poses a significant threat to the stability of financial systems worldwide and in Kenya, the challenge is no less daunting. The Institute of Certified Public Accountants of Kenya (ICPAK) stands out as a strategic partner in the war against money laundering and the recovery of proceeds of crime. As criminals become more sophisticated in concealing and legitimizing proceeds of crime, it is important that agencies mandated to fight these vices build strong alliances with professional institutions.

| The Strategic Role of ICPAK |

As the statutory body regulating the accounting profession in Kenya, ICPAK plays a critical gatekeeping role in ensuring financial integrity and ethical conduct among its members. Accountants, by virtue of their access to financial records, transactional data, and business operations, are uniquely positioned to detect anomalies indicative of illicit financial flows. Their professional vigilance, guided by the ICPAK Code of Ethics, can be instrumental in identifying suspicious activities at the earliest opportunity.

ICPAK also bears the responsibility of ensuring that its members comply with Anti-Money Laundering (AML) obligations under the Proceeds of Crime and Anti-Money Laundering Act (POCAMLA) by among others;

i. Reporting suspicious transactions to the Financial Reporting Centre (FRC) and other competent authorities.

ii. Developing and disseminating guidelines and best practices for Anti-Money Laundering (AML) compliance, to help accountants understand their obligations.

iii. Offering training programs and resources to educate accountants on AML regulations, red flags, and reporting procedures.

iv. Monitoring compliance with AML regulations among their members and may take disciplinary action against those who fail to comply.

v. Advocating for effective AML legislation and collaborate with regulatory bodies and law enforcement agencies to enhance the fight against money laundering.

| Who are the Other Reporting Entities? |

Designated Non-Financial Businesses and Professions (DNFBPs) such as accountants, lawyers, real estate agents, and dealers in precious metals and stones are classified as reporting entities. This classification also includes casinos, betting companies, and non-governmental organisations.

| Key Reports Submitted by Reporting Entities to the FRC |

Reporting entities are mandated to submit the following reports to the FRC:

▪ Cash Transaction Reports (CTRs) – These are filed for all cash transactions amounting to $15,000 (approximately KSh1.94 million) or more.

▪ Cross-Border Monetary Instrument Declaration Reports – These reports capture declarations by individuals crossing Kenyan borders while carrying currency or monetary instruments exceeding $10,000 (approximately KSh1.29 million).

▪ Suspicious Transaction Reports (STRs) – Filed whenever there is suspicion that a transaction, regardless of the amount involved, may involve proceeds of crime or be linked to money laundering or terrorist financing.

▪ Suspicious Activity Reports (SARs) – Filed to report unusual or potentially suspicious behaviour or activities that may indicate or facilitate illicit financial flows.

| Indicators that may flag a financial transaction as suspicious |

Financial transactions are considered suspicious when they deviate from expected patterns or lack a clear legitimate purpose. Common warning signs include;-

▪ Large cash deposits or withdrawals that are inconsistent with an individual’s known income or business operations.

▪ Attempts to avoid mandatory reporting thresholds such as by breaking up large sums into smaller transactions (a practice known as structuring).

▪ Unusual international money transfers, particularly those involving countries identified as tax havens or jurisdictions listed by the Financial Action Task Force (FATF).

▪ Rapid transfer of funds across multiple accounts without a justifiable economic reason.

▪ Clients who refuse to provide clear financial documentation.

▪ Clients using complex corporate structures with no clear business purpose.

▪ Discrepancies between declared income and observed financial behaviour

| What should Accounting professionals be doing to prevent money laundering |

i. Implement Strong Client Due Diligence (CDD) and Know Your Client (KYC) Measures by conducting rigorous background checks on clients including;-

▪ Verify Identities – Obtain government-issued IDs, business registration details, and tax personal identification numbers etc.

▪ Assess source of wealth – Require documentation proving where a client’s funds originate.

▪ Identify Beneficial Owners (BOs) – Ensure shell companies and corporate clients disclose true ownership.

▪ Apply Enhanced Due Diligence (EDD) for High-Risk Clients – Apply extra scrutiny for Politically Exposed Persons (PEPs), offshore entities, and high-value transactions.

ii. Maintain a robust AML compliance program by establishing internal policies and procedures to detect and prevent money laundering. Essential compliance measures include; –

▪ Appoint an AML compliance officer – A designated professional responsible for overseeing AML efforts.

▪ Undertake regular internal audits – Periodic reviews to ensure compliance with AML regulations.

▪ Maintain transaction records – Keep financial records and client documentation for at least seven (7) years.

▪ Mandatory employee training – Educate staff on AML red flags, reporting obligations, and compliance standards.

iii. Actively monitor client transactions and report any suspicious activities to the relevant authorities.

iv. Report suspected money laundering to the FRC and other relevant authorities.

v. Cooperate with law enforcement and investigative agencies by providing records and information as required.

vi. Uphold professional ethics and integrity avoiding conflicts of interest and reportingattempts of undue influence to facilitate illicit financial flows.

| Understanding Money Laundering |

Money laundering involves disguising the origins of illegally obtained money so that it appears legitimate. This process typically includes three stages: placement, layering, and integration. POCAMLA criminilizes money laundering under sections 3, 4 and 7 and imposes heavy penalties for both the offender and the enabler.

| The Role of the Assets Recovery Agency |

Mandate

The Assets Recovery Agency (ARA) is a body corporate established under section 53(1) of the Proceeds of Crime and Anti-Money Laundering Act, Cap 59B (POCAMLA). ARA mandate is to implement the provisions of Parts VII to XII of the POCAMLA. In particular, ARA combats money laundering, terrorism financing, proliferation financing through identifying, tracing, freezing and recovering proceeds of crime including profits or benefits derived thereof as well as assets used for or intended for use in the commission of a crime.

Functions

a. Identify and trace proceeds and instrumentalities of crime;

b. Institute court proceedings for freezing, seizure, preservation, forfeiture and confiscation of proceeds and instrumentalities of crime;

c. Co-operate with law enforcement agencies in recovery of proceeds of crime;

d. Manage seized, preserved and forfeited assets;

e. Administer the Criminal Assets Recovery Fund established under Section 109 of the Proceeds of Crime and Anti-Money Laundering Act, 2009; and

f. Provide international assistance in assets recovery investigations and proceedings.

| Assets Recovery Process |

The systematic process used to recover proceeds and instrumentalities of crime is as outlined below:

i. Reporting suspicious proceeds or instrumentality of crime – Citizens, public or private bodies can share a report via phone, email, online or anonymously through the Agency’s website. Report details to include the identity of the person, description of assets and nature of crime involved.

ii. Identify & Trace – Gather intelligence, investigate and uncover assets acquired through criminal activities or assets used to fund/facilitate criminal activities.

iii. Freeze & Seize – Obtain court orders to freeze/preserve or seize illicit assets, preventing them from being moved or hidden.

iv. Confiscate & Forfeit – Institute court proceedings to forfeit and confiscateproceeds and intrumentalities of crime to the Government.

v. Criminal Assets Recovery Fund (CARF)– The forfeited/confiscated assets are transferred into the Criminal Assets Recovery Fund and transmitted to the consolidated fund.

| Assets recovery legal regimes |

The Agency uses two assets recovery regimes namely; –

i. Criminal Forfeiture/confiscation (Conviction based recovery) where the suspect has to be prosectuted and convicted before instituting recovery proceedings.

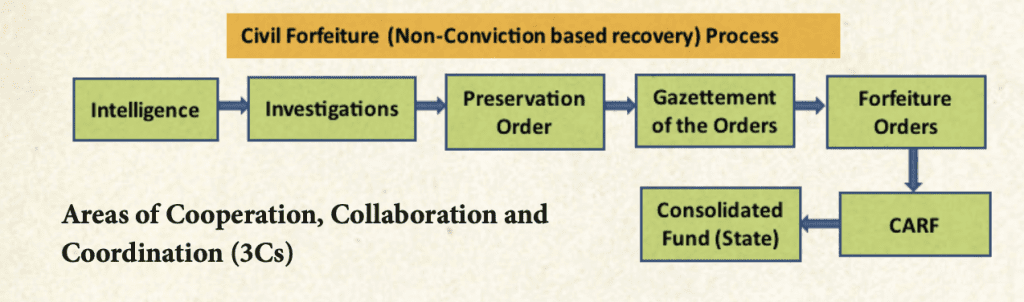

Civil forfeiture (Non-Conviction based recovery) which is not depended on criminal proceeding, criminal investigations to institute the proceedings or a conviction.

| Areas of Cooperation, Collaboration and Coordination (3Cs) |

ICPAK and the Assets Recovery Agency can synergize their efforts in the following pathways among others;

1. Information sharing and intelligence exchange – ICPAK and its members, under POCAMLA, are obliged to report suspicious transactions to the FRC and other authorities. The Agency can engage with ICPAK to develop early-warning systems and enhance information sharing.

2. Capacity building and joint training – Both institutions can co-develop training modules such as forensic accounting, asset tracing, and AML compliance among others. This would not only enhance the skills of ICPAK members but also provide Agency officers with insights into best accounting practices and red flags in financial statements.

3. Ethics and disciplinary support – ICPAK’s disciplinary mechanisms can be leveraged to ensure that members who enable or facilitate money laundering are held accountable.

4. Technical assistance in asset recovery cases – ICPAK can provide forensic accounting support by availing specialists to provide insights in complex asset tracing cases. Such technical collaboration can fast-track investigations and improve the evidentiary quality in asset recovery proceedings.

5. Public awareness and advocacy – Through its expansive network, ICPAK can help raise awareness among businesses, professionals, and the public about the importance of fighting money laundering and the role each stakeholder plays. Additionally, advocacy campaigns, publications, and symposia can amplify national efforts in combating illicit financial flows.

| Conclusion |

The fight against money laundering is a shared national responsibility that cannot be won in silos. The Assets Recovery Agency welcomes and values the partnership of professional bodies such as ICPAK in this endeavor.

We need to jointly build a resilient financial system that is hostile to money laundering and responsive to the aspirations of Kenyans for robust economy by leveraging ICPAK’s technical expertise, ethical standards, and professional networks.

In forging this alliance, we will not only enhance the Agency’s operational efficiency, but also affirm a shared commitment to combating these vices and promoting good governanceand the rule of law in the country.

Mark M. Ogonji, EBS, OGW, ‘ndc’(K) Ag. DIRECTOR GENERAL