By Jim McFie, a Fellow of ICPAK

There Are Rapidly Escalating Impacts of Climate Change

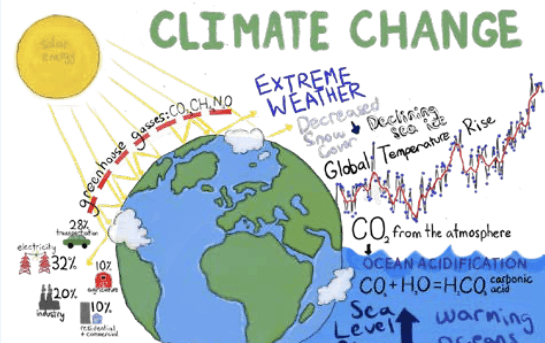

The International Federation of Accountants (IFAC) has just published two documents on aspects of Sustainability Reporting: the first document concentrates on Greenhouse Gas Reporting. IFAC states that mandatory greenhouse gas (GHG) reporting is imminent. IFAC and four sustainability oriented organizations, We Mean Business Coalition (WMBC), Accounting for Sustainability (A4S), Global Accounting Alliance (GAA), and World Business Council for Sustainable Development (WBCSD), have released guidance to help chief financial officers, accountants and finance professionals build on existing systems and processes in order to undertake or enhance cost-effective and investor-grade GHG reporting. The first publication is an eight-page document entitled “8 Steps to Enhance GHG Reporting: A Roadmap for Accounting and Finance Professionals”. This paper points out that there are rapidly escalating impacts of climate change and mandatory requirements are looming that will require companies to disclose robust information about their GHG emissions and climate risks and opportunities. As a result, the IFAC and the group provide finance and accounting professionals with a roadmap to engage with others across their business to prepare for GHG emissions reporting requirements aligned to financial reporting processes.

This first document equips accountants with the technical guidance necessary to collect and enhance the quality of data related to all aspects of GHG emissions at individual entity and group levels. When IFAC states that enhanced GHG reporting will be required by regulators, it is reminding us that this is happening in a number of capital markets already. Not only that, but IFAC realizes that the upcoming international and jurisdictional standards and regulations that will make it mandatory for companies to advance GHG reporting to new levels and provide investors with decision-useful information related to climate risks and opportunities. These include the International Sustainability Standards Board (ISSB) General Sustainability-related Disclosures (IFRS S1) and Climate-related Disclosures (IFRS S2), the European Financial Reporting Advisory Group’s (EFRAG) European Sustainability Reporting Standards (ESRS) and proposed rules for climate change disclosures by the U.S. Securities and Exchange Commission (SEC). In Kenya, companies listed on the Nairobi Securities Exchange (NSE) are now required to report on their Environmental, Social and Governance (ESG) activities in accordance with the NSE publication “Nairobi Securities Exchange ESG Disclosures Guidance Manual November 2021”, but there is no requirement in this document to report on GHG emissions. A useful reference document for GHG reporting is “The Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard”.

The Greenhouse Gas Protocol Initiative is a multi-stakeholder partnership of businesses, non-governmental organizations (NGOs), governments, and others convened by the World Resources Institute (WRI), a US-based environmental NGO, and the World Business Council for Sustainable Development (WBCSD), a Geneva-based coalition of 170 international companies. Launched in 1998, the Initiative’s mission is to develop internationally accepted greenhouse gas (GHG) accounting and reporting standards for business and to promote their broad adoption. The GHG Protocol Initiative comprises two separate but linked standards: firstly, the GHG Protocol Corporate Accounting and Reporting Standard (this document, which provides a step-by-step guide for companies to use in quantifying and reporting their GHG emissions); and secondly, the GHG Protocol Project Quantification Standard (a guide for quantifying reductions from GHG mitigation projects: this standard has not yet been published although there is a GHG Protocol for Project Accounting).

This GHG Protocol Corporate Accounting and Reporting Standard provides standards and guidance for companies and other types of organizations preparing a GHG emissions inventory. It covers the accounting and reporting of the six greenhouse gases covered by the Kyoto Protocol — carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulphur hexafluoride (SF6). The standard and guidance were designed with the following objectives in mind: (1) To help companies prepare a GHG inventory that represents a true and fair view of their emissions, through the use of standardized approaches and principles; (2) To simplify and reduce the costs of compiling a GHG inventory; (3) To provide the business with information that can be used to build an effective strategy to manage and reduce GHG emissions; (4) To provide information that facilitates participation in voluntary and mandatory GHG programs; (5) To increase consistency and transparency in GHG accounting and reporting among various companies and GHG programs. Both business and other stakeholders benefit from converging on a common standard. For businesses, it reduces costs if their GHG inventory is capable of meeting different internal and external information requirements. For others, it improves the consistency, transparency, and understandability of reported information, making it easier to track and compare progress over time.

The business value of a GHG inventory Global warming and climate change have come to the fore as a key sustainable development issue. Many governments are taking steps to reduce GHG emissions through national policies that include the introduction of emissions trading programs, voluntary programs, carbon or energy taxes, and regulations and standards on energy efficiency and emissions. As a result, companies must be able to understand and manage their GHG risks if they are to ensure long-term success in a competitive business environment, and to be prepared for future national or regional climate policies. A well-designed and well-maintained corporate GHG inventory can serve several business goals, including: (1) Managing GHG risks and identifying reduction opportunities; (2) Public reporting and participation in voluntary GHG programs; (3) Participating in mandatory reporting programs; (4) Participating in GHG markets; and (5) Recognition for early voluntary action.

The GHG Protocol for Project Accounting (Project Protocol) provides specific principles, concepts, and methods for quantifying and reporting GHG reductions— i.e., the decreases in GHG emissions, or increases in removals and/or storage—from climate change mitigation projects (GHG projects). The Project Protocol was the culmination of a four-year multi-stakeholder dialogue and consultation process, designed to draw knowledge and experience from a wide range of expertise. During its development, more than twenty developers of GHG projects from ten countries “road tested” a prototype version of the Protocol, and more than a hundred experts reviewed it. The Project Protocol’s objectives are to provide a credible and transparent approach for quantifying and reporting GHG reductions from GHG projects, to enhance the credibility of GHG project accounting through the application of common accounting concepts, procedures, and principles, and to provide a platform for harmonization among different project-based GHG initiatives and programs. To clarify where specific actions are essential to meeting these objectives, the Project Protocol presents requirements for quantifying and reporting GHG reductions and provides guidance and principles for meeting those requirements. Though the requirements are extensive, there is considerable flexibility in meeting them. This flexibility arises because GHG project accounting necessarily involves making decisions that directly relate to policy choices faced by GHG programs—choices that involve tradeoffs between environmental integrity, program participation, program development costs, and administrative burdens. Because the Project Protocol is not intended to be biased toward any specific programs or policies, the accounting decisions related to these policy choices are left to the discretion of its users.

One difficulty in any business is who should take the lead in GHG action and reporting. “Organizations need to determine who will be accountable for setting the reporting strategy,” says a partner in a Big Four firm. Although finance professionals have not historically taken on this responsibility, many believe it is critical for them to do so as more and more companies embrace GHG reporting as a strategic asset. With the need to disclose risks and opportunities, the finance function and its external auditor are best positioned to lead reporting and deliver success for an organization. Finance is uniquely positioned because it is familiar with and has the ability and access to collect information across the organization to meet reporting requirements. Furthermore, finance professionals understand how to convert GHG metrics into financial reporting language and financial metrics through their experience in compiling and reporting other information. Financial, accounting and auditing professionals can assist the entire organization education — educating internal and external stakeholders on GHG topics about where a company is in its GHG journey, where it wants to be and how to get there; governance — participating in cross-functional steering committees and working groups; strategy — developing a clear reporting strategy that provides consistent, comparable, timely and decision-useful information; risk assessment — determining the specific areas that are relevant for a business; controls — leveraging previous reporting experience in other areas to establish reliable and tested processes; and finally reporting — delivering thorough and reliable reporting.

The second document just published by IFAC, “GHG Reporting Building Blocks for Accountants,” relies heavily on what I have just covered above. It equips accountants with the technical guidance necessary to collect and enhance the quality of data related to all scopes of GHG emissions at individual entity and group levels.

Kenya’s tree cover, according to the World Bank data, currently stands at 6.3%. If we follow the President’s suggestion of growing (not merely planting) trees, we will play our part in dealing with GHG. One of the foods for trees is CO2: if we grow trees, they will do the GHG work for us.