In section: sponsored feature

By CPA Majani Derrick

As new businesses are created and old ones spun off, processes evolve, technologies are adopted, and regulatory demands fluctuate, the internal audit function must develop new approaches to advise management on key issues, anticipate risk and be more forward-looking. Changes like these call for innovation on a significant scale. A framework for innovation can be helpful in ensuring the necessary steps are completed in a logical order. One such framework is Doblin’s1 Ten Types of Innovation®, which can provide internal auditors with a practical model to support the rigor and quality of their innovation efforts.

Applying the Ten Types of Innovation Framework

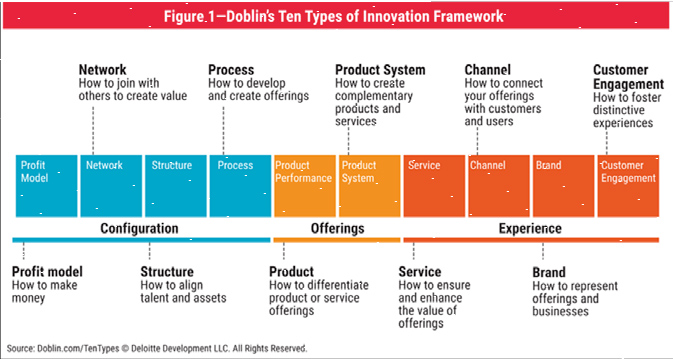

The Ten Types of Innovation framework, shown in figure 1, is a flexible approach to innovation that is highly applicable to internal audit. The framework is especially suited for situations in which incremental innovation is preferable to radical change created in isolation. The framework’s phases enable teams to develop concepts that will be relevant to stakeholders. They guide the research process and marshal insights to generate offerings that produce value for customers or stakeholders. In the final phase, the team refines its concepts to generate an actual service offering. The Ten Types of Innovation framework lends structure to the innovation process, which helps allay concerns about the disorder and risk that can sometimes accompany significant change.

The framework’s phases enable teams to develop concepts that will be relevant to stakeholders. They guide the research process and marshal insights to generate offerings that produce value for customers or stakeholders. In the final phase, the team refines its concepts to generate an actual service offering.

Setting Innovation Strategy Working with the chief audit executive and other internal audit leaders, internal audit gauges the external and organizational environment, identifies areas where stakeholders would benefit from innovation, and aligns initiatives with needs. Potential questions to address include:

- Integrated—Innovation in internal audit must be integrated with the organization’s goals and strategy, and calls for adopting the language of business

- Iterative—Organized iterations enable internal audit to hone new approaches, learn through experience, build trust among stakeholders and proceed at a comfortable pace.

- Incremental—Incremental change goes hand in hand with an iterative approach in setting reasonable expectations and in establishing a feedback loop with stakeholders as initiatives proceed.

- Independent—It is critical that internal audit preserves its independence as it pursues innovative approaches. Its intent should be to improve its own processes for meeting stakeholders’ needs.

- Independent—It is critical that internal audit preserves its independence as it pursues innovative approaches. Its intent should be to improve its own processes for meeting stakeholders’ needs.

Setting Innovation Strategy

Working with the chief audit executive and other internal audit leaders, internal audit gauges the external and organizational environment, identifies areas where stakeholders would benefit from innovation, and aligns initiatives with needs. Potential questions to address include:

- How should internal audit define innovation?

- How can internal audit become more aligned with business goals and strategy?

- Where in the organization could stakeholders most benefit from innovative solutions?

- What are the best ways to discover stakeholders’ most pressing needs?

Becoming Better Innovators Internal audit helps cultivate new methods within the function—from protocols and metrics for managing the innovation portfolio to talent development and knowledge transfer. Internal audit also alerts the business to potential connections with external organizations to assist in sustaining innovation. In this phase, those in the internal audit function should ask themselves:

- How can internal audit best structure and organize innovation?

- How can the function create clear and useful objectives for innovation?

- What will spur stakeholders to support these innovation efforts?

Designing, Building and Launching Innovations

After evaluating insights from within the function and from other key stakeholders, internal audit helps prioritize opportunities and develop a plan for capitalizing on them to improve audit outcomes. Questions that the internal audit function can ask to help move it toward this stage include:

- How can internal audit create deeper value, rather than only deliver changes to processes and deliverables?

- How can the function manage the risk of innovating through pilot projects, diversification and other methods?

- How will internal audit know whether improvement has been achieved?

By configuring elements among the Ten Types of Innovation framework, internal audit can alter its approach to internal audits, its service offerings or the stakeholder experience to create new outcomes to contribute to the organization’s success. The framework could be augmented by workshops to develop specific initiatives or entire programs that align with management’s goals and the organization’s needs. Such workshops also could help create action plans related to stakeholder expectations, team capabilities, change management and facilitation needs. A structured, outcome-focused approach to innovation typically resonates with internal audit and its constituents, including chief financial officers (CFOs) and audit committees. By managing the innovation process effectively, internal audit can position itself to identify promising opportunities and be the spark to innovate with discipline.

1 Comment

Interesting article. I am generally critical whenever concepts are hyped. Innovation is one such theme. The danger with hype and models or frameworks is one akin to buying a hammer then looking for nails to hit. This is best exemplified in the ‘Setting Innovation Strategy’ section, third bullet question. “Where in the organization could stakeholders most benefit from innovative solutions?”

Under the ‘Setting Innovation Strategy’ section, the second bullet question is excellent. “How can internal audit become more aligned with business goals and strategy?” The answer may or may not lie in innovation!

I have had an experience where an Internal Audit function acquired a data analytics tool then started looking for audit procedures to apply the tool. Totally unacceptable!